Inside Reddit's ARPU Engine (RDDT)

The 6th most visited website on the internet is still dramatically under-monetized. Base case 7x in operating profit by 2028 for a 35% 3-year IRR.

Reddit is a rare beast as far as ‘social media’ platforms go.

You cannot realistically compare it against other public social media companies like Snapchat, Meta, or Pinterest. Why is that?

Reddit is a forum-of-forums, made up of over 100,000 individual subreddits that are created, maintained, and moderated by their own users. Subreddits are much more effective at filtering for high-quality, human generated information (which is the crux of much of this thesis) than other social media platforms for a few key reasons:

Subreddit mods mandate that content stays clean and crucially, on-topic

Reddit users filter posts with ‘upvotes’ and ‘downvotes’ instead of a simple like button — low quality spam content is downvoted and automatically filtered out

Reddit is primarily anonymous. This empowers users to have open, honest conversations that could not occur on socials like Instagram, where your profile is tied to your name, where you live, and all of your friends. You can speak your mind on Reddit in ways that you can’t do on other platforms, which brings in valuable and honest perspectives.

Reddit is text-based which allows for a more ‘conversational’ format than Instagram, where 90% of users go to watch funny short-form content and post their vacation pictures once a year. Those honest, human conversations are what create so much value for advertisers and data-mining AI companies. As AI slop becomes increasingly proliferated in the coming years, this authenticity will make Reddit even more valuable to users, advertisers, and AI companies themselves.

Reddit executives stated on the Q4 2025 call that they will soon roll out flagging and verification of 3rd party bot accounts (Reddit uses their own bots for subreddit moderation). Their CEO literally used the phrase ‘AI slop’ on the call; they are plainly going to continue prioritizing human-generated content and weed out bots by any means necessary, which is crucial to preserving authenticity.

Reddit has been under-monetized for decades.

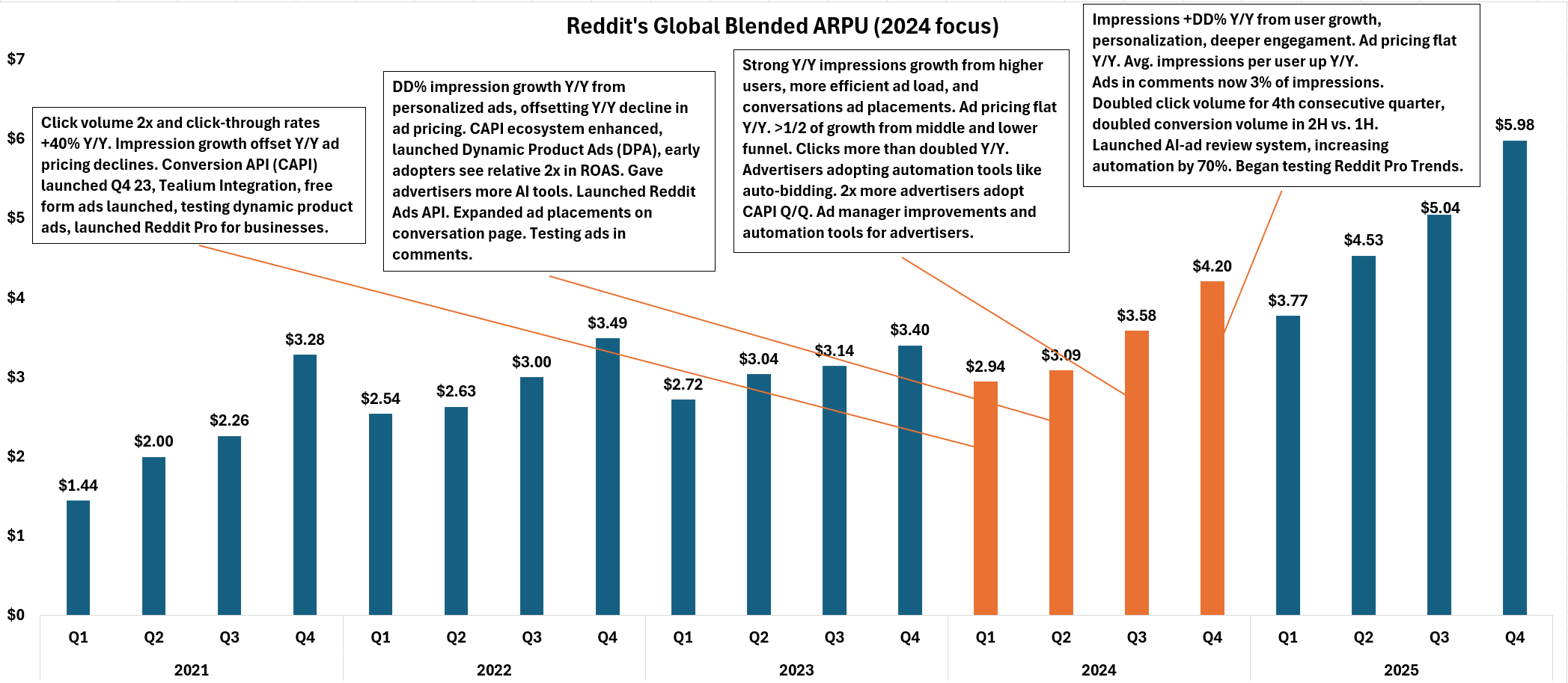

That is starting to change, but I don’t think most market participants realize how far the ARPU (average revenue per user) ceiling can go, even after their ARPU has grown by nearly 2.2x since 2021 and accelerated meaningfully in 2025. I also doubt most people realize how much forward ARPU growth is essentially locked in today, and how much the company is doing to increase ARPU.

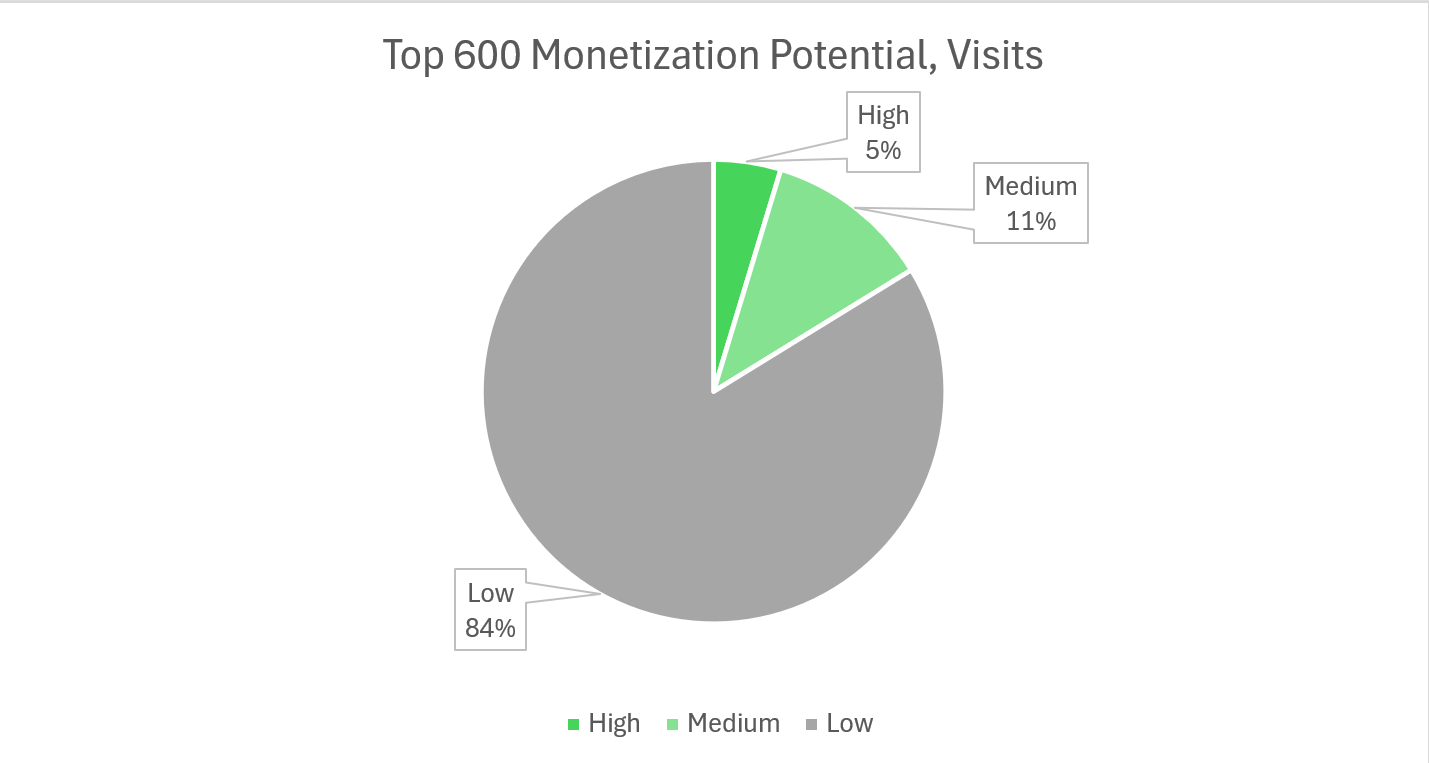

To understand how high the ARPU ceiling is, I manually scraped data from the top 600 subreddits ranked by membership, weekly visits, and weekly posts, and classified each subreddit based on a qualitative monetization potential score between Low, Medium, and High. You can read about my scoring methodology and the other nitty-gritty stuff in the Index section at the bottom of this piece.

I estimate that this dataset covers at least 14% of Reddit’s total traffic. That does not seem like a large number, but given the inclusion of 600 of the most subscribed and most active subreddits, I think it should be fairly representative of Reddit as a whole.

Anyway — we can glean from this that roughly 16% of Reddit’s traffic is medium-high monetization potential, which means they see higher CPMs (cost per thousand impressions) than low-tier filler ad inventories which are common on most entertainment and news sites. It’s hard to find exact figures but I would naturally assume this is a higher share of high-intent traffic than is seen on almost any other website besides Google itself.

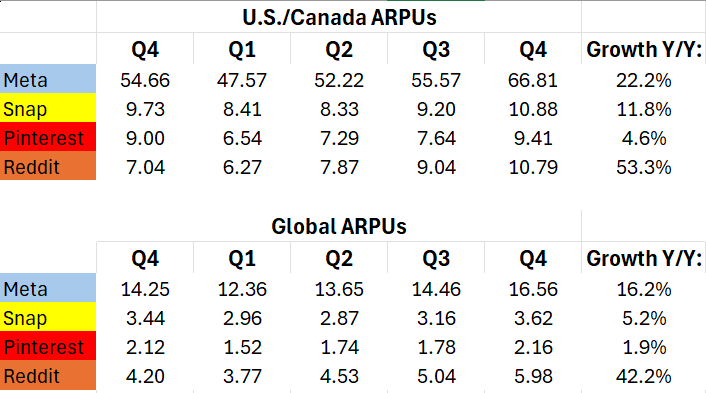

The comparison between Reddit and other social media platforms is striking; Pinterest for example arguably has higher purchase intent. Users go there primarily to shop or to assemble sorts of shopping lists, but these are limited to lower-ticket retail and CPG goods like home furnishings. Take a look at this comp sheet:

Pinterest is the closest comparable based on platform dynamics and ARPUs. But judging by growth rates, Reddit is absolutely steaming past them. How can this be, if Pinterest has higher purchase intent traffic on average?

It all depends on what is being sold. On Pinterest it’s mostly retail and CPG as I’ve said. But people go to Reddit for things like financial and legal advice, gaming PCs, laptops, quality headphones, and other high-ticket hardware recommendations, among many other categories.

Reddit excels in providing consumers trust in community sentiment, a place where people go to research what the best laptop is for the price. Whatever day you read this, the exact phrase “best laptop reddit” has been Googled about 50 times, for example. More on this, later.

That is a phenomenon that is unique to Reddit. You don’t go to Instagram, Twitter, Pinterest, or Snapchat for that sort of thing. High-ticket items need more research, more trust put into them before consumers are willing to cough up that kind of money. Reddit’s communities naturally build that trust through honest, human discussions. That is what makes Reddit so valuable.

Cranking ARPU

We’ve established that Reddit has built a lot of trust as a research destination for consumers who are in the final stages of making a purchase decision or otherwise have higher than normal purchase intent.

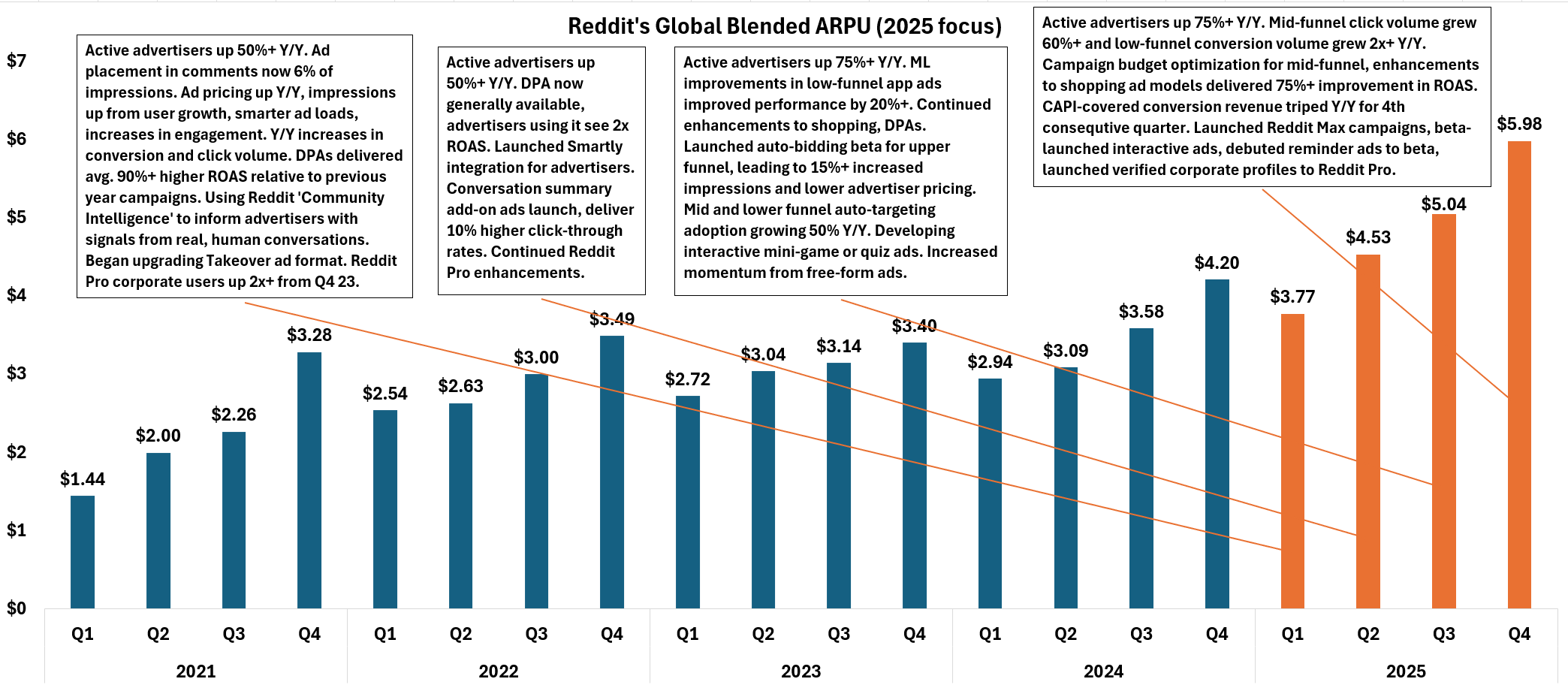

We know Reddit has a solid share of traffic to valuable, high CPM destinations. We know they should and will soon see structurally higher ARPU than all comps except Meta. What is Reddit doing to exploit this unique advantage? All the right things. Let’s take a look.

You will have to zoom in, but you’re going to want to read the callouts on each of these slides. I cannot understate the degree to which Reddit’s management have already done much of the initial work to improve the ad ecosystem, and that we are still in the early stages of this growth.

Let’s start out with their CAPI revenue coverage stats. CAPI stands for Conversion API, a tool that lets advertisers know when they actually make a sale because of a Reddit ad. Historically this tracking has been done by simpler, less capable cookie-based ‘Pixel’ systems.

These systems are much more proliferated than Reddit’s CAPI at 90% revenue coverage, because they are much easier for advertisers to implement than CAPI, which can require some manual setup and server integrations between Reddit’s servers and advertiser servers.

Thanks to Apple’s enhanced user privacy programs, most IOS users now opt out of data tracking, which cuts Pixel off from IOS data and makes it significantly less effective for advertisers to check actual sales from Apple ecosystems, which are responsible for an appreciable share of overall traffic, estimated at 30%+ of high-CPM traffic (U.S. IOS Ecosystem users).

If advertisers can’t see whether or not their ads are driving sales in 30% of cases, they’re simply not going to spend as much on ads. It’s not worth shooting in the dark any more than you have to when working with large ad budgets, right? You could be lighting money on fire and you wouldn’t even know it.

Reddit’s CAPI launched in Q4 2023 to a small base of advertising customers, we can estimate something around 1-2% to start out. Based on their callouts, CAPI-adopting advertisers quickly doubled Q/Q in Q3 2024, bringing the total to an estimated 5% of advertisers using CAPI.

They also called out that CAPI-covered revenue tripled Y/Y each quarter in 2025. Bridging from Q3 2024, let’s say CAPI-covered revenue in Q3 2025 was 15% and to be conservative, let’s say 20% in Q4. Crucially, on the latest call their COO said the following:

“I think the team is doing a great job shouldering something like CAPI that doesn’t drive revenue today.” - Reddit COO Jennifer Wong, Q4 2025 earnings call

Advertisers with CAPI tracking enabled are going to spend more on ads. If it doesn’t drive revenue today, that means the vast majority of advertisers (the number of which is still growing >50% Y/Y) have not yet adopted this solution that we know is only going to increase spend per advertiser through better tracking and advertising purchase attribution. Reddit has a stated goal of 100% of customers adopting CAPI, and they are clearly making great headway.

This is just one source of ARPU growth. Within these earnings callouts Reddit literally has broken down for us, multiple sources of compounded ARPU growth that are only in their early stages of adoption.

What other metrics can we look at? Let’s hone in on ROAS (return on ad spend) and active advertiser counts. Much like Meta and other advertising networks, Reddit ad pricing is determined by advertisers bidding in the marketplace of available ad inventory.

If advertisers see higher ROAS, they’ll bid higher for more ads, pushing ad pricing up. If more advertisers join the platform as well (active advertisers grew over 50% each quarter in 2025), you can just imagine how that increases liquidity and price discovery in Reddit’s ad marketplace.

If you have ROAS go >2x from certain ad formats, as was called out with DPAs in Q2 25, the advertiser marketplace will slowly see that ROAS lift, bid up pricing on those ads, and eventually theoretically pricing would double to match ROAS, sort of arbitraging away any extra return above some market baseline in terms of ROAS. Additionally, in Q1 25 it was called out that DPAs generated 90%+ higher ROAS compared to prior year campaigns.

Effectively ad pricing in their higher conversion formats could double, which likewise doubles ARPU in those formats. The rollout of these ads has already started but they are not nearly fully proliferated — interactive ads for example have higher conversions than basic formats, and those just went into beta testing in Q4 25.

“You saw our strong growth in retail that’s fueled by the success we’ve been seeing in DPA. Now it’s very early, there’s a lot more advertisers and a lot more opportunity there.” - Reddit COO Jennifer Wong, Q4 2025 earnings call

Dynamic Performance Ads, DPAs, are Reddit’s ML-enabled solution to targeted ads, offering dramatic increases in targeting capability for the mid and lower funnel, which are much higher CPM than top of funnel ads. This kind of dramatic improvement in ROAS for the lower funnel specifically is where you start to see CPMs put up crazy growth numbers, leading to massive ARPU expansion.

DPAs automatically generate personalized ads by pulling data from an advertiser’s product catalogue, and dynamically recommending these products to users based on the extensive data that Reddit can gather on each individual user.

For example, I can make a new account today and go join a few subreddits that are relevant to me, like r/Austin, r/securityanalysis, and r/PCgaming. Immediately based off my own self-selecting into certain subreddits, Reddit knows I live in Austin and I like stocks and PC gaming. Reddit also knows what users post, comment, and how often they interact with certain subreddits.

Now with DPAs, Reddit and their advertisers can actually take advantage of that information that historically has not been leveraged in this way. This is how Meta, Google and others generate such high ARPUs, they leverage information on users to dynamically target them with relevant ads.

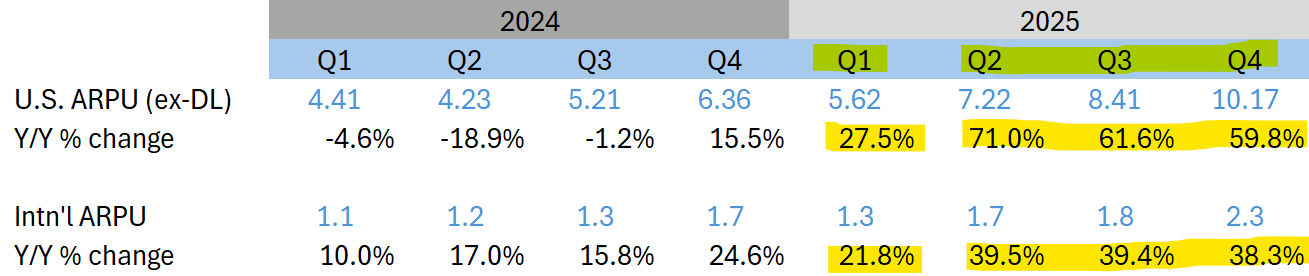

DPAs specifically have been performing incredibly well both in the U.S. and internationally. In Q2 2025 when DPAs were released to general availability, you can actually see Y/Y ARPU growth rates for all geographies double, just like that. Following the pattern of advertisers seeing 2x higher ROAS —> advertisers spending 2x the amount on ads —> ARPU doubles (roughly).

Given how much the ad ecosystem can still be improved, U.S. ARPU growth rates accelerating to +60% Y/Y in Q4 2025, and Reddit’s ~15% share of high purchase-intent traffic based off my data scraping, I am suggesting that Reddit is almost guaranteed to see vastly higher ARPUs once these advertising solutions are further adopted.

In 2025, Reddit’s annual ARPU for U.S. users was $33.97. Contrast that to Meta, which saw a staggering $212 in annual ARPU from users in the U.S. and Canada in 2025. Reddit could triple their U.S. ARPU and still only be halfway to Meta’s U.S. ARPU.

Meta’s ARPU is so high because of their incredibly sophisticated ad targeting algorithms, enhanced with over a decade of machine learning progress to be incredibly accurate, even if their share of high-medium intent traffic is probably lower than Reddit’s with lower CPMs on their highest-ticket items (you’re not buying software licenses or PC parts on Instagram). You buy different things on Meta, but Meta is just a lot better at selling them. Meta also has a higher ad load than Reddit generally across products like Instagram, further boosting their ARPU.

I believe I recently found Reddit increasing the ad load in their main ‘For You’ equivalent feeds in IOS, from one ad every nine posts to one ad every seven-eight posts on average. I ran three trials at different times, waited a few days, and ran more trials — these later trials showed the increased ad load. Ramping the ad load from one every 9 posts to one every 7.5 posts results in a 20% effective increase in impressions.

They may just be testing things out here, so I’ll be waiting to see if they call this out on the Q1 call. But if they did indeed increase the ad load, that is 20% of essentially free impressions and ARPU growth that will be locked in for 2026. Reddit’s previous ad load at one every nine was so light that the increased load should have almost no effect on user experience. I only noticed it because I was specifically checking to measure it.

Considering these factors, it is abundantly clear that Reddit is well on it’s way to dramatically increasing advertising ARPU beyond the 2.2x growth we have already seen since 2021. I am suggesting a U.S. ARPU target of 1/2 Meta’s current U.S. ARPU, which would be an increase of 3x to $102 annually.

Data Licensing Upside

Currently, Google pays Reddit $60mm annually in data licensing contract revenue, and OpenAI pays about $70mm. That is some pretty small potatoes compared to the $30Bn OpenAI is projected to make in revenue this year alone, with at least $20Bn coming from consumer ChatGPT subscriptions.

Reddit is cited in 40% of all AI queries — it is the single most cited source. AI models scrape Reddit’s data, aggregate it, organize it, and feed it to consumers through their text responses. If 40% of that data comes from Reddit (said another way, 40% of the value to the end user), that means Reddit will in part enable about $8Bn in consumer ChatGPT subscription revenue in 2026, not even counting the advertisements that ChatGPT is beginning to roll out to free users. The $70mm Reddit keeps today is a measly 0.86% of that.

Reddit executives aren’t blind to this — the licensing contract with Google was signed before Reddit went public, and the OpenAI contract was signed a few months after going public. Crucially, both of these contracts were inked before any of us knew how AI would change online consumer behavior.

In late 2025 Reddit began re-negotiating their data licensing contracts with Google and OpenAI early, per Bloomberg, seeking significantly more money or potentially (and much more excitingly) an ongoing usage-based model, where Reddit will get a bigger kickback for providing data to queries where their data is uniquely valuable. No matter what, they are going to raise the price of their uniquely valuable data, likely by a very significant margin.

The contracts with OpenAI and Google will expire in late 2026 and early 2027. I expect Reddit to grab a lot more price upon re-negotiations and I would be frankly ecstatic if a usage-based model is adopted. As mentioned above, Reddit executives came back to the negotiating table a year early and they are hungry for more price.

If Reddit increases the price of their data, where else can AI providers go?

Well, Google has YouTube data — text or speech within YouTube videos as well as text in comments. The size of this database is enormous and is continually updated with 720,000 hours of new video content uploaded each day. This will end up being hugely valuable for Google, but it says a lot that Google has this resource and still pays Reddit for data.

But Anthropic and OpenAI for example don’t have a YouTube. All the web data they use, they will need to get from somewhere, and a solid percentage of it will always come from Reddit, which continually produces enormous volumes of the highest-quality human-generated data.

Funnily enough, Anthropic and OpenAI put together control at minimum 60% of the consumer AI market. Google has some of their own data and has recently taken share from OpenAI, but the other ~60% of the market does not. You see what I’m getting at here — I think Reddit has ample room to make data licensing a much bigger business than it currently is today, as AI companies cannot realistically recreate the volume and quality of Reddit’s data on their own.

If we want to assume a usage-based model and Reddit captures just 5% (up from my estimated 0.86% today) of the consumer AI revenue they help generate for OpenAI alone, their data licensing segment could triple in sales from $130mm today to $400mm, an expansion that falls entirely to the bottom line as data licensing is effectively 100% margin, almost pure income. During FY 2025, Reddit’s total earnings were $530mm, so you can see why this gets me so excited.

Is a 5% value capture realistic? I think in time, genuinely yes. But there are some slight risks. OpenAI and Google already paid up for Reddit API access, but Anthropic and Perplexity have not and are currently being sued by Reddit for the unauthorized collection of data without permission.

Each of these companies accessed Reddit’s data after being asked to stop. Anthropic said they stopped, but allegedly did not, accessing Reddit’s data over 100,000 times unauthorized. Perplexity continued accessing Reddit’s data through Google search results after being handed a cease-and-desist.

In Perplexity’s case, Reddit engineers literally set up a honeypot with targeted information and found that same information within Perplexity’s AI models within hours, again, after a cease-and-desist order. I think Reddit has a pretty a strong case.

These lawsuits were filed mid-late 2025 and will likely see progress in mid-2026, though timelines are uncertain. The resolutions here may not even matter. If OpenAI and Google, which collectively are over 80% of consumer AI market share are already paying up, one could argue the others will eventually follow suit anyway and that the lawsuits do hold water.

Theoretically Reddit could pull some backend shenanigans to make it nigh impossible for AI scrapers to access their data, if the lawsuits fall through and AI companies don’t want to pay up. The historical record favors holders of proprietary data being able to successfully monetize that data. I’m obviously betting on Reddit’s case here.

On User Growth Concerns

One thing that has weighed on investor confidence in Reddit recently has been concerns over slowing growth in some user segments. I think these fears are wildly overblown for the following reasons.

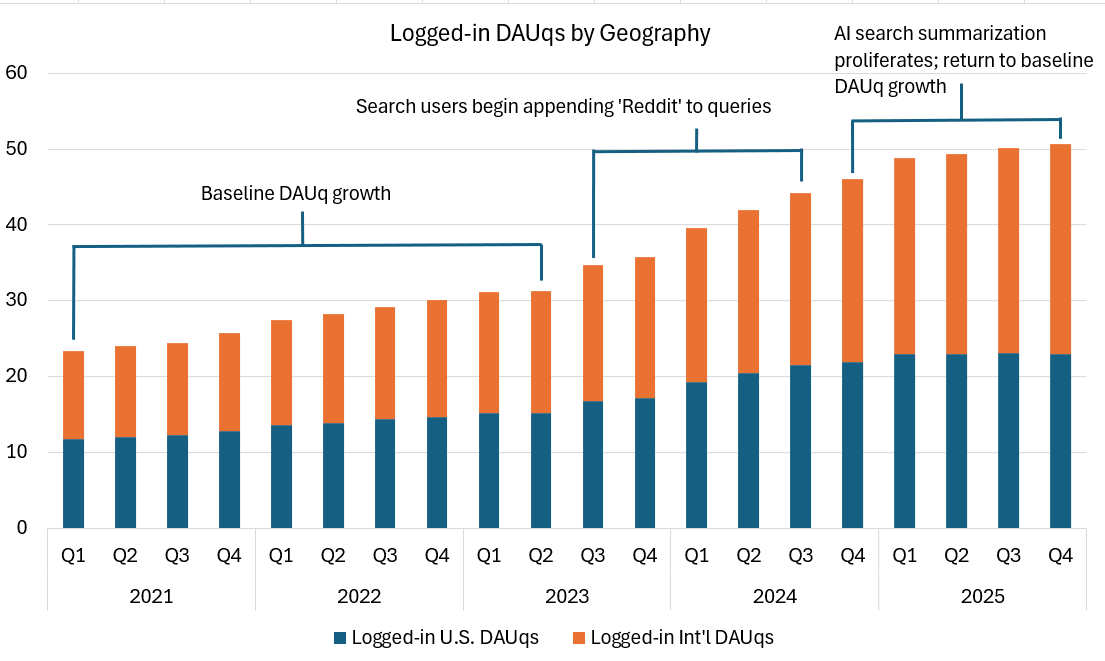

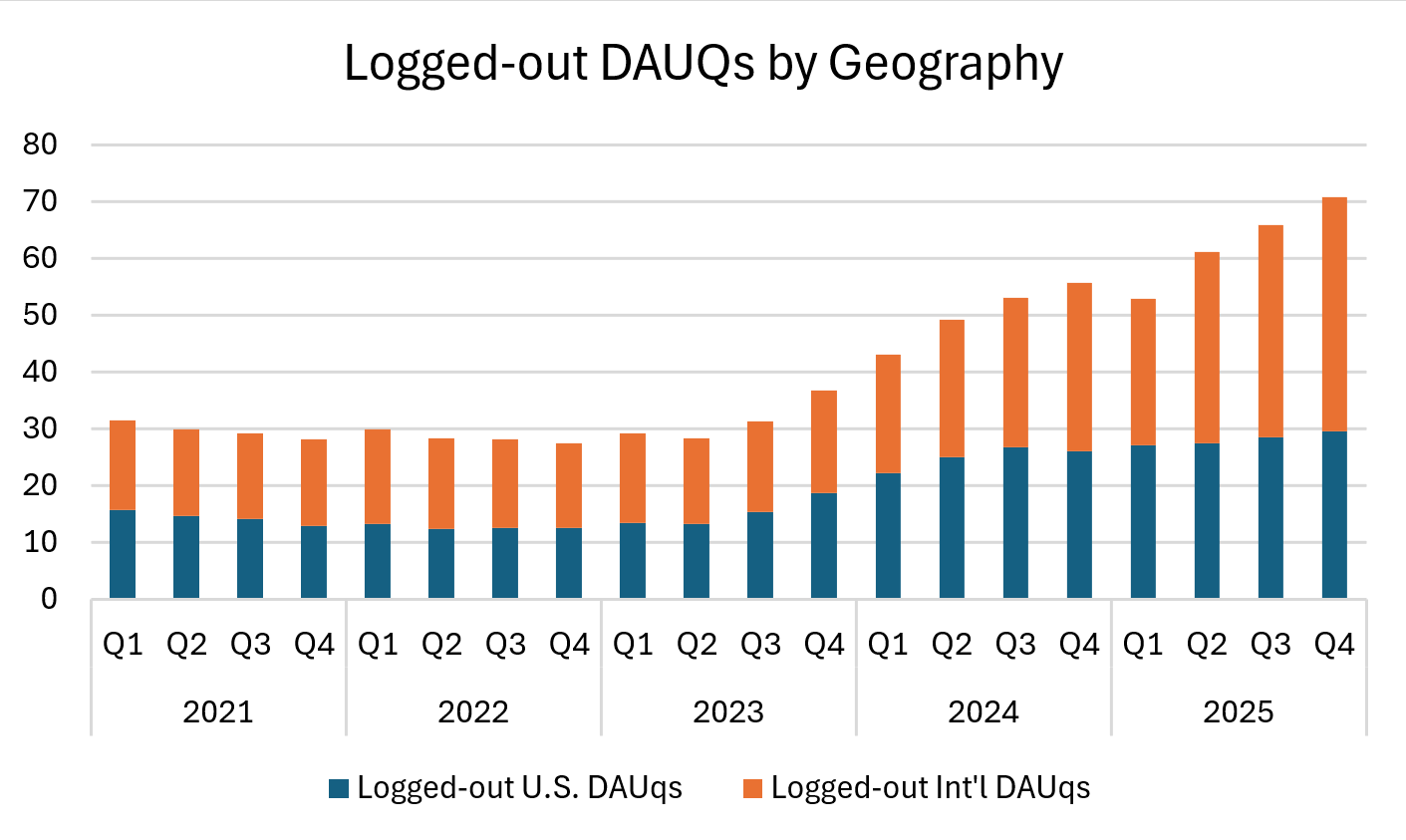

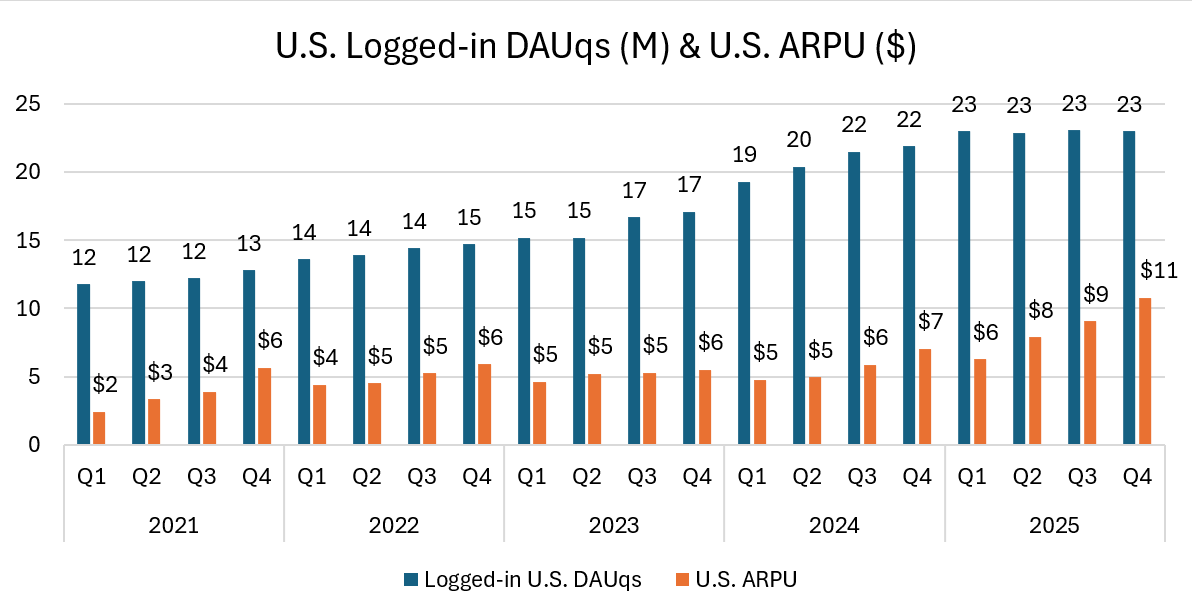

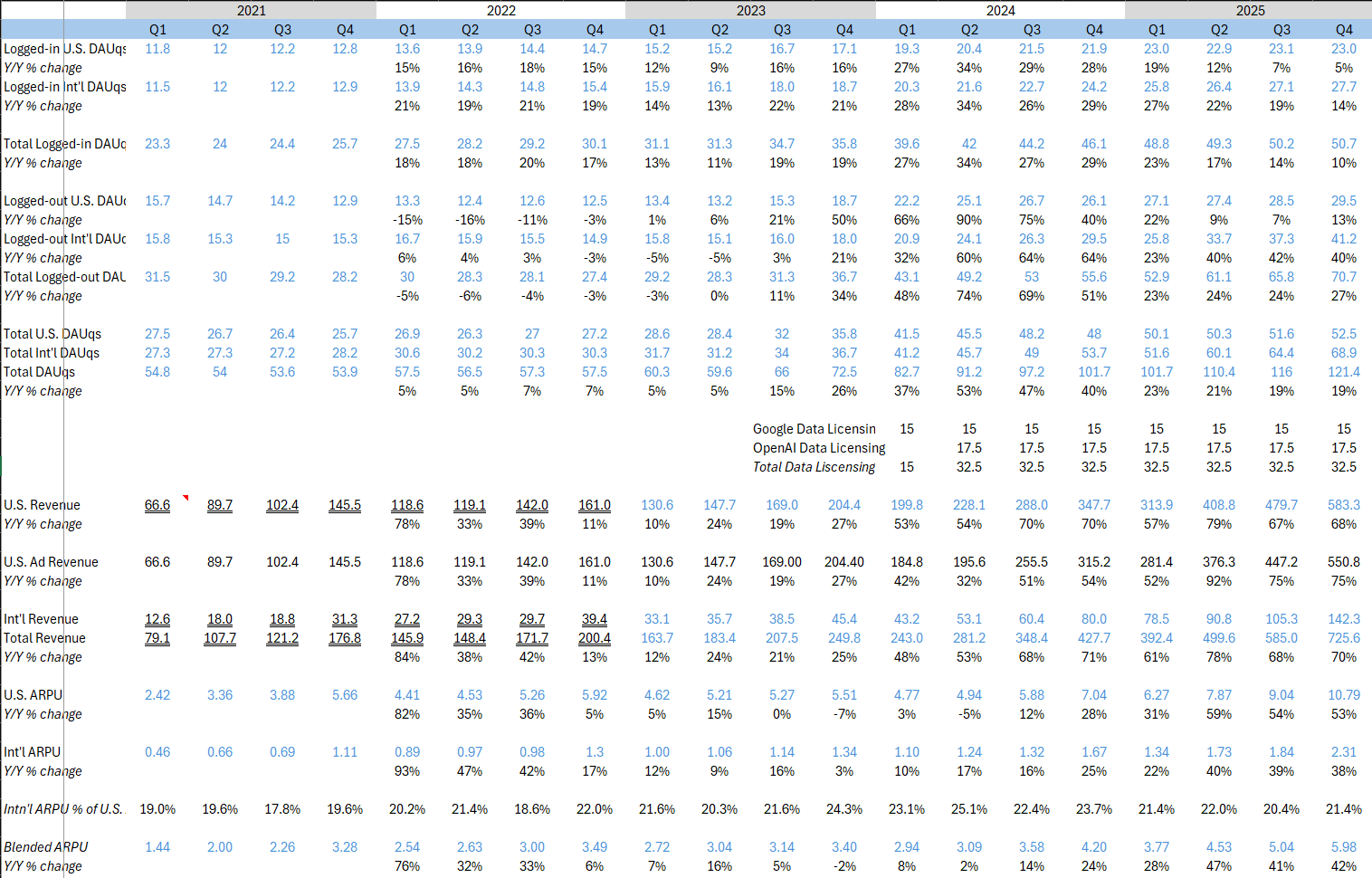

This chart shows the number of logged-in vs. logged-out DAUqs (daily active unique users) by geography. Logged-in users are more monetizable than logged-out users, and currently international ARPU is only 21% that of U.S. ARPU.

The best user cohort to grow is logged-in U.S. users, as they are the most monetizable cohort. These users have hovered at flat around 23 million for the past 4 quarters straight. Is this concerning for growth? I do not think so, and you can see my reasoning is in the chart above. I think after AI search summaries, Reddit has more or less returned to its previous ‘baseline’ low growth rate.

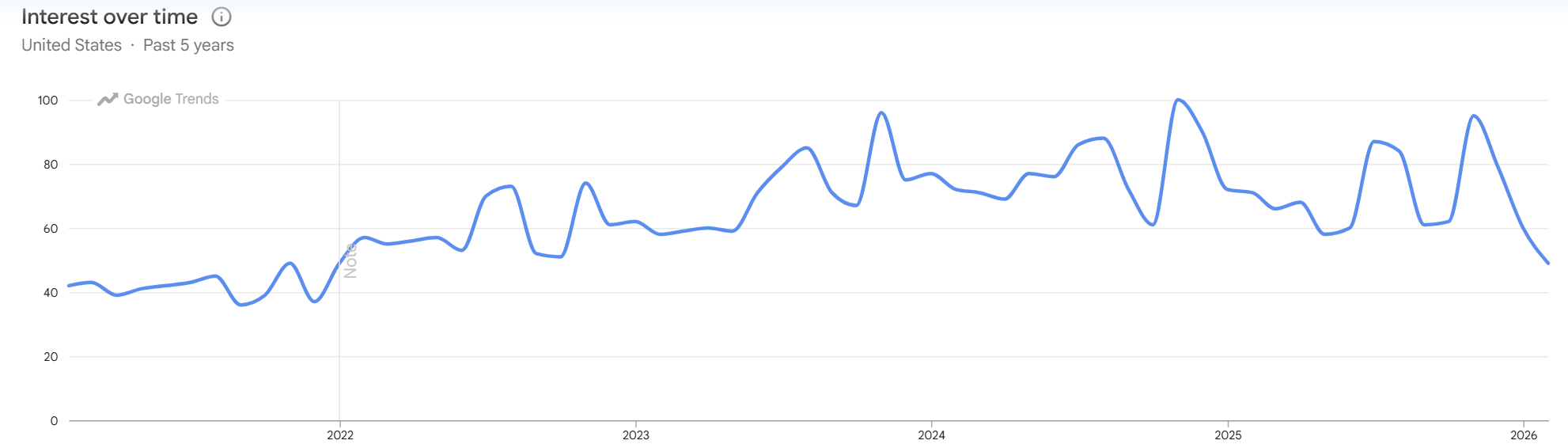

This hypothesis is also supported by Google Trends data. Here’s that ‘best laptop reddit’ search query volume I mentioned we’d come back to earlier on:

You can see Trends follows a similar pattern to the first chart in this section. Increasing search queries in 2023 and 2024 brought more new users, and since then AI summaries have decreased that effect, leading to lower growth. I myself have followed this exact pattern of user behavior and I’d bet that many of you have as well.

Here is their growth in logged-out users by location:

In a similar story to logged-ins, international logged-out users are growing much faster but overall users are still growing. Now, why does the slowing growth of logged-in users not actually matter?

My ARPU estimation essentially mandates that ARPU is going to increase very substantially purely from existing ad ecosystem improvements that have yet to be fully realized. User growth is of course not required for growth in either advertising ARPU or data licensing. Reddit is going to continue putting up nutty topline growth numbers (with a heap of operating leverage) even if you assume zero growth in users. Even so, Reddit executives may have a solution to the “AI growth-stealing” problem.

Per Bloomberg, in the ongoing AI contract re-negotiations mentioned above, Reddit executives are considering a model that incentivizes AI providers to resume steering some traffic back toward Reddit, instead of taking the majority of would-be traffic in their Google search summaries and AI query responses.

This is speculation from me, but I see a future where Reddit charges higher dynamic usage-based prices for its data in AI queries across the board, and will waive or slash fees for queries in which the AI models provide limited information to users and instead say, “You can read more about this topic on this Reddit thread [link].”

That would represent a true win-win. Reddit gets more traffic, and AI companies will have a cost incentive to provide it. This would likely help return Reddit to its recent higher rates of logged-in user growth.

Another concern of many market participants is that beginning in Q3 2026, Reddit will stop disclosing the split between logged-in and logged-out users. While some concern is warranted, I do not actually think this change is very material. As Reddit executives argue, the distinction is beginning to matter less and less as Reddit gets better at serving targeted ads to logged-out users who briefly browse Reddit sentiment before making a purchase decision.

Another thing I want to point out is that Meta doesn’t report the split between logged-in vs. logged-out users. Honestly, in comparison Meta’s disclosures are somewhat of a black box. Meta is a machine that spits out increased user growth and increased ARPU like clockwork, and you don’t see people questioning them for that. The distinction between logged-in vs. logged-out users decreases at scale — either way, Reddit is seeing higher repeat traffic that they are only going to get better at monetizing.

Here is the same information in chart form. User growth in U.S. logged-in is absolutely not required for Reddit to continue cranking ARPU (well, by definition) and massively increasing sales at 60%+ incremental margins.

Financials and Modeling

We’ve got the revenue drivers (ARPU, Data Licensing) put together, now let’s do some income statement modeling. I’m gonna hit you in the face with this right now, my base case is a 7x in operating profit within 3 years. I know that sounds insane so let me walk you through it.

Firstly, to make a point I am assuming user growth will be flat, even though it is most definitely going to continue growing overall. I don’t think it’s too important to this thesis and going without it bakes in some conservative assumptions.

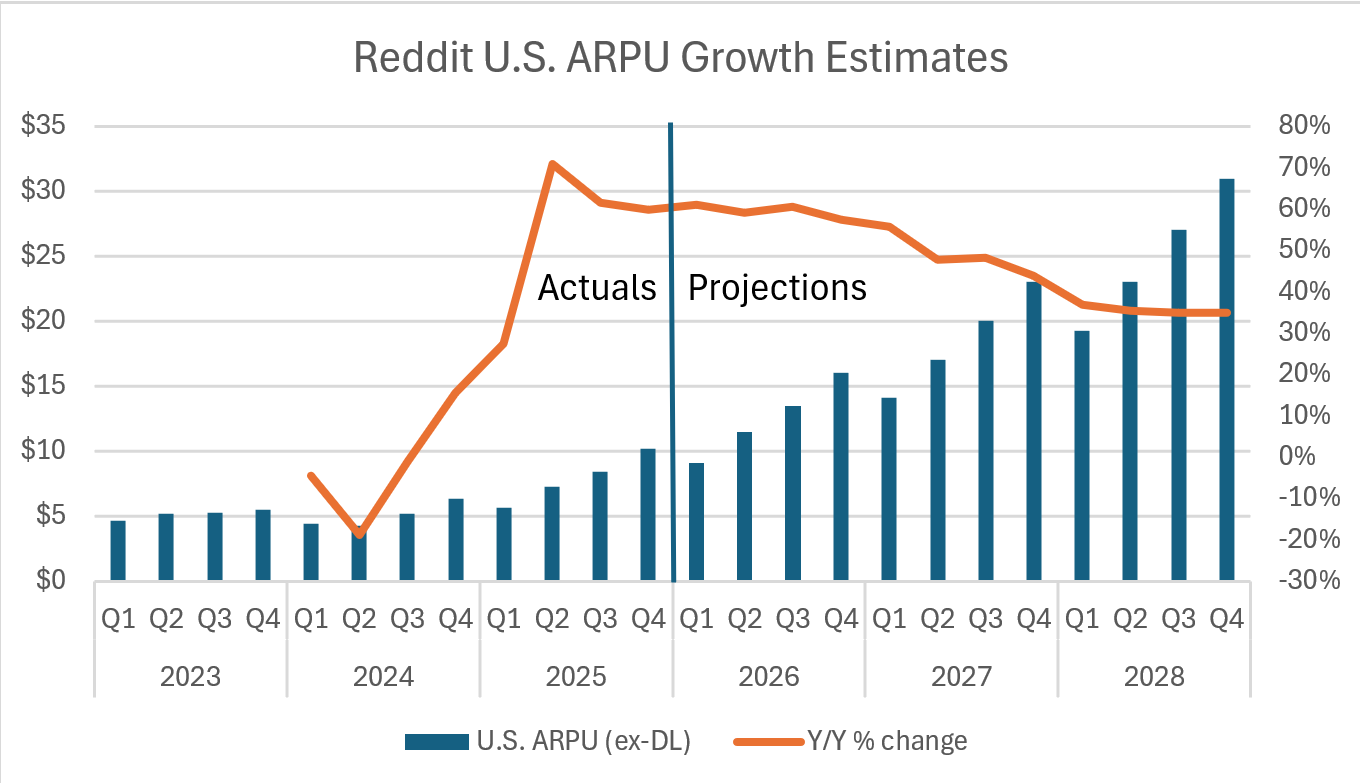

Secondly, U.S. ARPU is the most important driver here. I have it increasing at about 60% in 2026 (same as every quarter in 2025 since DPAs were launched to general availability), 50% in 2027, and 35% in 2028. The end result of that is, 2028 annual ARPU lands dead-on $100, half of Meta’s current U.S./Canada annual ARPU. I have Reddit’s international ARPU falling from 21% of U.S. ARPU to 19% by 2028 as the international growth rates are slower.

Is that defensible? Maybe I’m crazy, but I do think so. Firstly — as mentioned earlier, I think Reddit simply has higher CPM, higher purchase intent traffic than Meta and others on average as my data scraping seems to indicate.

Also, that $100 U.S. ARPU target for Reddit is just in the U.S. — Meta’s $200 figure for the U.S. and Canada of course includes Canada, which isn’t as maniacally consumerist as the U.S. is, so maybe we could assume Canada’s ARPU would be 85% that of the U.S., that would put Meta’s pure U.S. ARPU even higher.

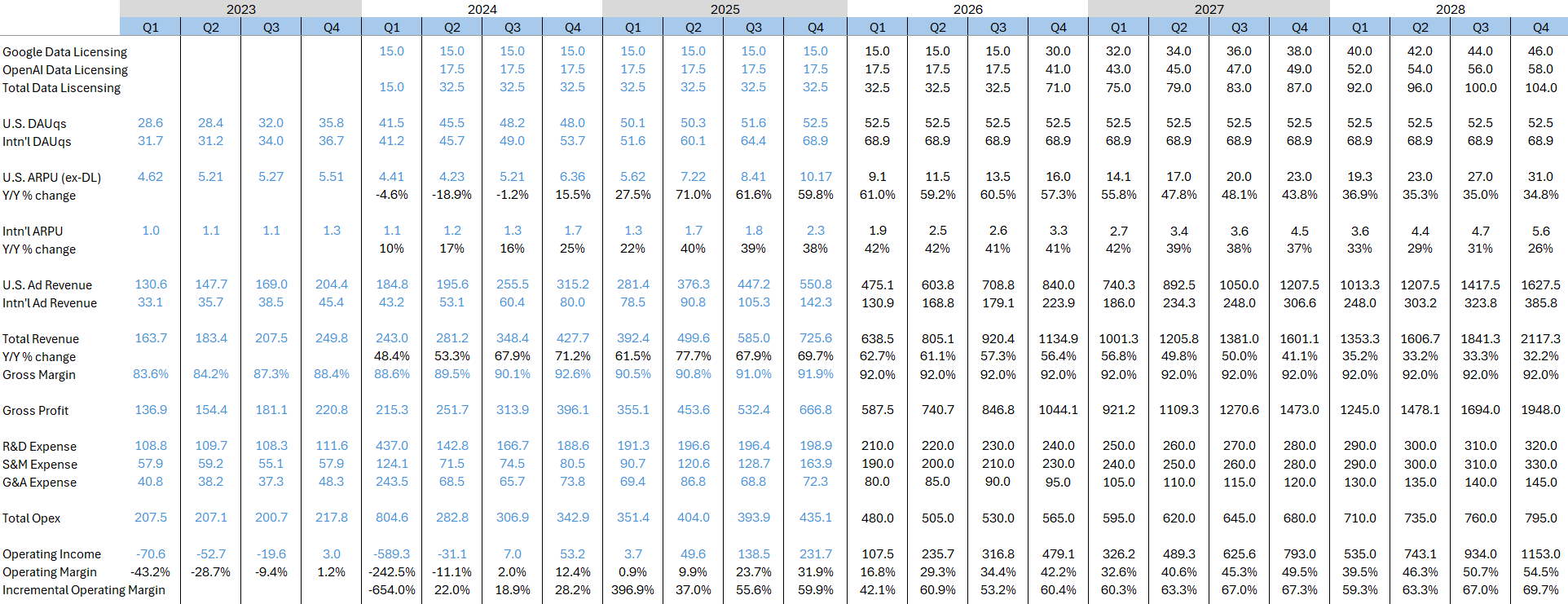

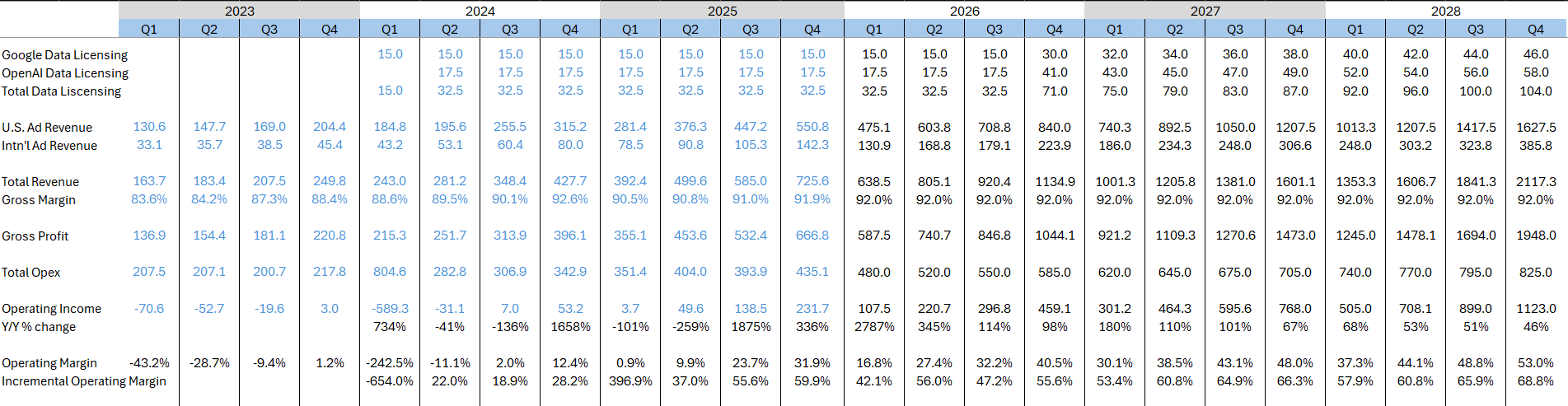

Here’s the raw model:

Here’s an easier-to-digest view of the most important metrics:

I have Google data licensing revenue doubling and OpenAI licensing revenue increasing 2.5x, with small quarterly escalators baked into each to approximate a usage-based model. Google data licensing doesn’t grow as fast as OpenAI because I believe Google is getting better at aggregating data from YouTube and they simply won’t need as much of Reddit’s data as OpenAI will.

Potential Perplexity and Anthropic contracts are not included. This is a lower value capture rate than the 5% I penciled in for the earlier Data Licensing Upside section. Even if I’m wildly off on data licensing, by end 2028 it represents only 5% of sales. So, it doesn’t matter too much and if anything I think there could be serious upside to these numbers.

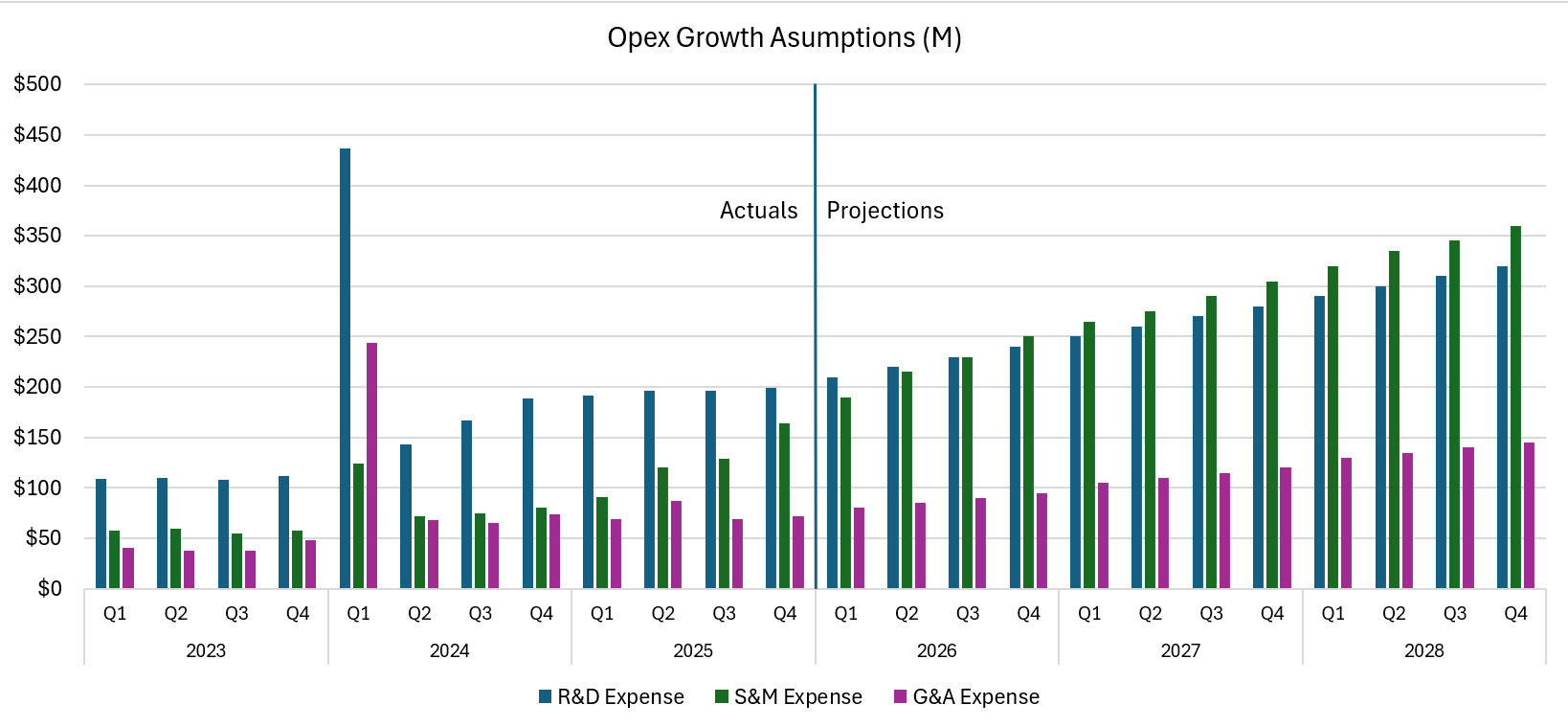

I’m pretty confident in my ARPU and revenue modeling, so here’s a sanity-check of my opex modeling:

To be conservative I have R&D and G&A expenses growing demonstrably faster than they did in 2025, offset by a slight normalization in the S&M growth rate as Reddit’s sales force matures and productivity scales. Overall opex grows roughly by 30%, 25%, and 20% in 2026, 2027, and 2028 respectively.

I have Reddit exiting 2028 at a 46% EBIT margin and I expect that Reddit’s terminal margins will approach Meta’s current 60% advertising EBIT margin some time after 2028 given that Reddit’s gross margin is about 10% higher and I have not identified any drivers that could lower it.

Additionally, Meta likely spends between $5-10Bn annually on content moderation, whereas Reddit’s moderation is handled almost entirely at the subreddit level by over 50,000 volunteer moderators equipped with automated tools like the AutoMod bot. That’s at least a few points worth of structural extra margin that Reddit has above Meta.

Why is this model, despite forecasting a 7.6x increase in EBIT in only 3 years, still arguably conservative? Because it focuses solely on ad targeting and personalization ARPU (specific ARPU growth rates attributable to DPAs and other targeting and format improvements), and does not bake in any increases in impressions (increased ad load called out earlier, user growth) that are likely going to meaningfully contribute further to growth.

If the 20% increase in ad load I caught is genuine, if ads in comments continue increasing impressions, if users continue to grow (all of these are highly likely) revenue could compound at meaningfully higher rates than I’m estimating.

At the end of it all, today Reddit is trading at 8x EV / 2028 EBIT based on my numbers (and current 28Bn market cap - 2.5Bn cash, no debt). You could cut my EBIT estimates in half and still earn a market rate of return assuming a 20x EV / EBIT exit multiple (a 3.5 turn contraction from today’s fwd 2026 multiple).

Any way you slice it, that 8x 2028 is a dirt cheap multiple for something with this growth and margin profile. Applying a more reasonable 20x EV / EBIT exit multiple to my projected 2028 run-rate EBIT numbers results in a ~35% three-year IRR.

If you consider that ending 2028 these projections show Reddit at $3.2Bn run-rate EBIT growing 45% at nearly 70% incremental EBIT margins, and apply a higher 30x EV / EBIT exit multiple instead, your three-year IRR is 55%.

Reddit’s management team know that their shares are wildly underpriced. A director recently purchased $7mm of shares in the open market, increasing her stake by 600%. That’s a pretty big vote of confidence.

With their Q4 2025 earnings Reddit’s BoD has also approved a $1Bn share repurchase program with no set expiration date, representing about 3.5% of the market cap. The 1.5% dilution they are guiding for 2026 could be easily cancelled out, and then some, and this demonstrates confidence in the long term-durability of the company’s earnings.

Risk Factors

The most relevant risk factors include:

A slowdown in the economy could worsen the advertising environment and stunt Reddit’s rapid growth

While I think it is unlikely, Reddit’s userbase could revolt at some scale if management pushes the ad load or other monetization efforts too far, too fast

Reddit may not be able to go back to it’s previous high-user growth range, and in what I’d consider to be a very unlikely scenario user growth may reverse

Reddit may not be able to manage it’s costs as effectively as I predict and I would be overestimating the degree of operating leverage in the business

If Reddit loses the AI data mining lawsuits, they may not see as much or any upside from data licensing contracts

Conclusion

This pitch is free to read. If you like my work and want to support me, it would mean a lot if you like, retweet, or re-stack this post so it can catch more eyes. I’m also currently in the market for a buyside equities internship, if any fund managers or analysts happen to be reading this… please shoot me a DM on any platform if you like this work and are interested in connecting.

Thanks for reading. Have a great day. I’ll be writing you all again sometime soon!

Index

This section contains all the KPI data I have gathered on Reddit along with my traffic monetization database and methodology. Have fun… I know I did putting this together.

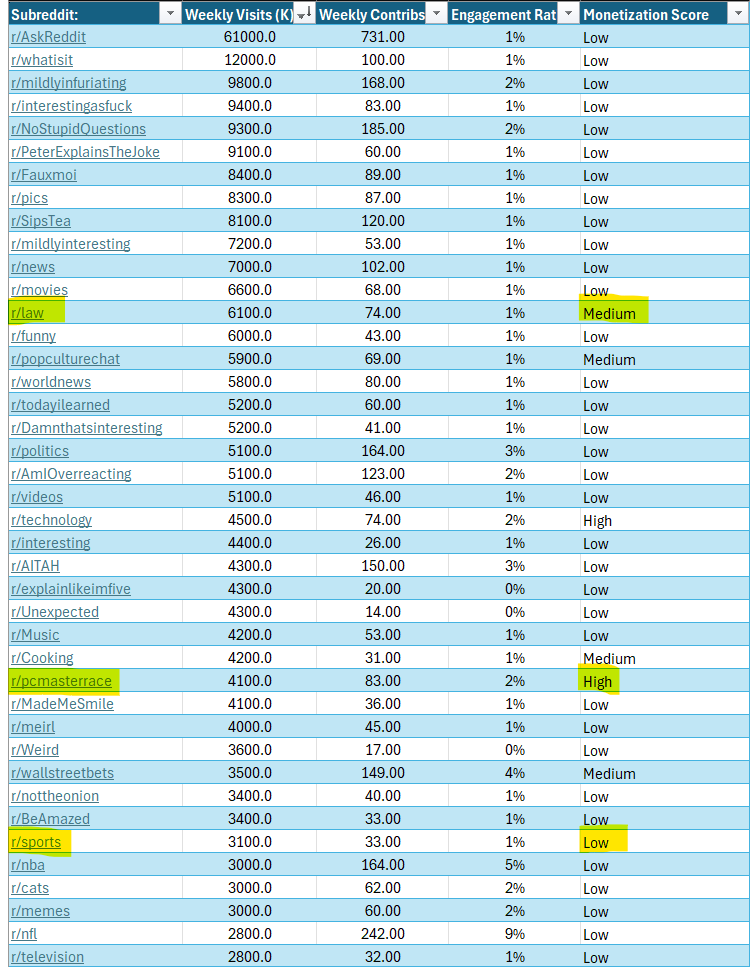

Monetization scoring methodology and data coverage:

Monetization scoring reflects typical online advertising CPMs for subreddit related content (finance/tech higher, news/politics lower), as well as assumptions about the user group within certain subreddits. Specific methodology follows:

High scores:

r/PCBuild — Users are seeking recommendations and inspiration to build their own PCs, a very high-CPM category as PC parts cost hundreds/thousands of dollars and the subreddit itself is very targeted towards that niche.

r/HomeImprovement — Users are looking for home improvement recommendations and may be served targeted ads for high-ticket power tools, or for stores like Lowes and Home Depot.

r/Golf, r/Cruise — the types of people regularly playing golf and buying cruise tickets are guaranteed to be higher income on average than the average user of subreddits like r/Funny. Thus, advertising slots in these subreddits should command premium CPMs (though of course inventory in these subreddits is limited with traffic).

Medium scores:

r/Running — Users are primarily there to discuss running, but they may happen to be interested in ads for a new pair of high-ticket running shoes, or maybe hydrating sports drinks or other related products.

r/Recipes — Users are primarily there to discuss cooking and recipes, but they may be interested in ads for cookbooks, grocery delivery, or kitchen gadgets and high-ticket accessories like fancy knives, air fryers, and etc.

Low scores:

The majority of Reddit discussions (news, politics, sports, memes/humor) is rated as low, because users are typically there for entertainment, not to make or consider purchase decisions. Low-scoring subreddits include r/politics, r/dadjokes, and r/cats (among very many others).

I estimate this dataset captures about 14% of Reddit’s total traffic. Total weekly subreddit visits in this dataset are 612 million and weekly contributions (posts and comments) are 9.8 million. Weekly numbers are based on a 28-day moving average and calculated by Reddit itself. Annualized, that is 31 billion individual subreddit visits and 508 million contributions. In total, Reddit saw about 3.75 billion contributions in 2025, hence my 14% coverage estimate.

Obviously this is not perfect coverage, but it would be physically impossible for me to get data on all 100,000 subreddits and there are no other free sources for this data, believe me, I checked. The top 600 most subscribed subreddits will have to do.

Here is a sample of this dataset ranked by subreddit weekly visits. I’ve highlighted more examples of the Monetization Score methodology as well. This is just a small sample, keep in mind this contains data from 600 individual subreddits.

Broader KPI Tracking

Really impressive writeup. Thanks for sharing.

Biggest risk is Meta waking up and outcompeting them like they did to Snap. Not super likely though