Welfare Weekly - Edition #1

Portfolio updates & weekly basket performance - first edition of Welfare Weekly!

See the not financial advice disclosure at the bottom of this article.

Portfolio updates:

Added Marex (MRX) at 11% weighting, a financial services firm specializing in clearing, execution, market making, and tailored hedging/investment solutions. A recent-ish IPO (nearly a year ago to the day), Marex has demonstrated some extremely impressive performance relative to other small caps, as seen below:

Shares have doubled since their IPO from $19 to $42, helped by 50% net income growth in 2024.

I have this at a pretty big weighting, but I’m no stranger to buying into strength in new names - really, I’ve been looking for this sort of company all year so far. I think it could do really well in this market, given it’s high growth, relatively low valuation, competent management team with high ownership, strong business fundamentals with high barriers to entry, and global revenue diversification. I love these sorts of financials businesses, it reminds me of IBKR in a lot of ways, even though they operate in different parts of the financial ecosystem value chain. I’m going to conduct more research on this name over time - I’m planning for this to be a long term hold and I wanted to get my foot in the door early.

What I like about Marex:

UK-based, NASDAQ listed, a recent IPO, a small company ($3Bn marketcap) that not many people are following, thus a very reasonable valuation of ~12x forward earnings (15x TTM) - pretty darn cheap for the growth that these guys have been putting up

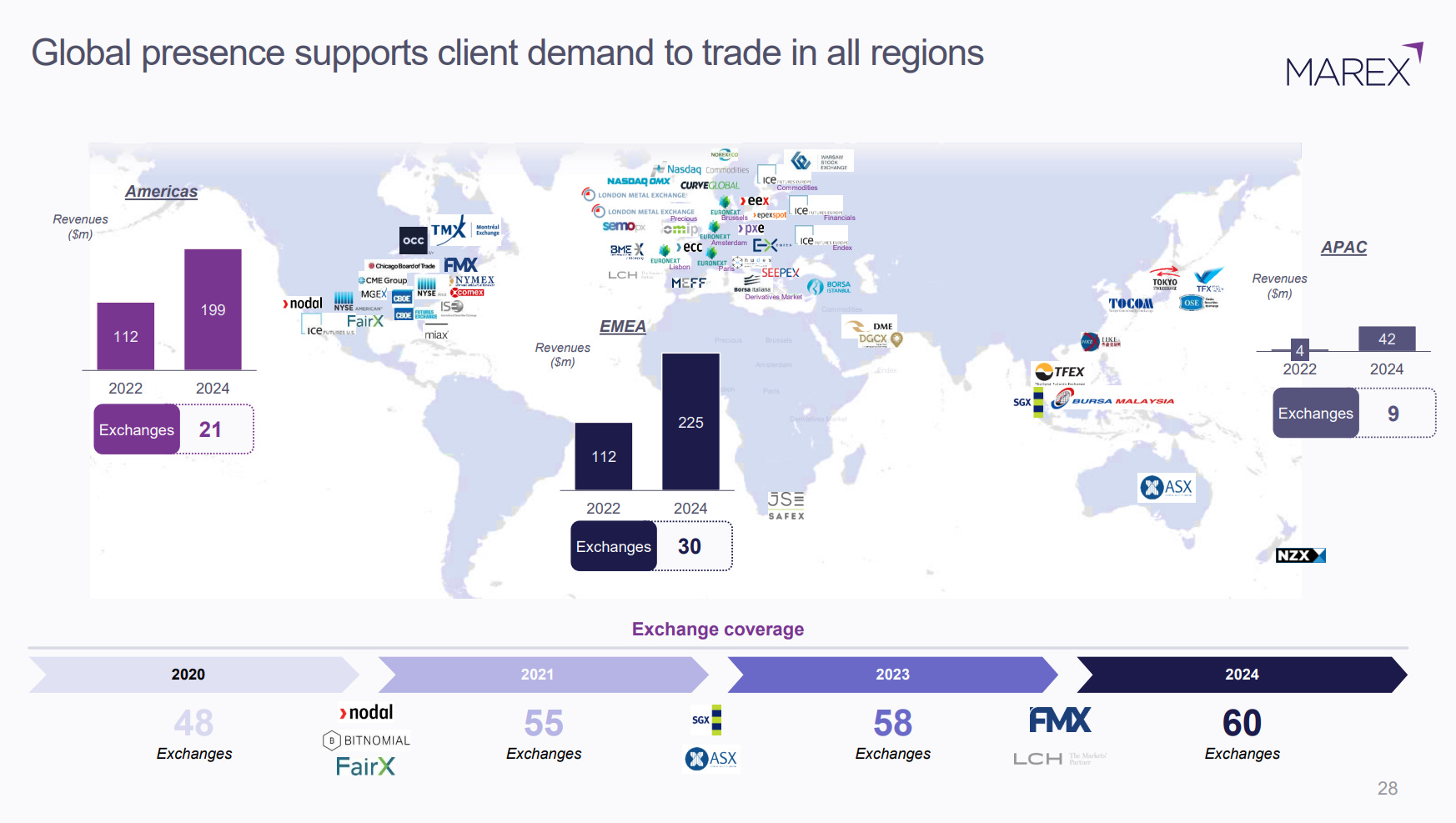

Globally diversified revenues: 36% from the Americas, 56% from EMEA, and 8% from APAC regions, if US macro uncertainties continue (which I think they will), Marex is more insulated than many other US listed companies

Management own around 50% of shares so they’re well aligned, and knowledgeable about their own business - how they can keep growing, how they can expand margins, the barriers to enter their environment, what their clients need, etc

Management knows how to talk to investors and they had a recent (April 2, 2025) Investor Day - their investor materials are really quite good, and I think increased awareness of this company can continue leading to better share price performance

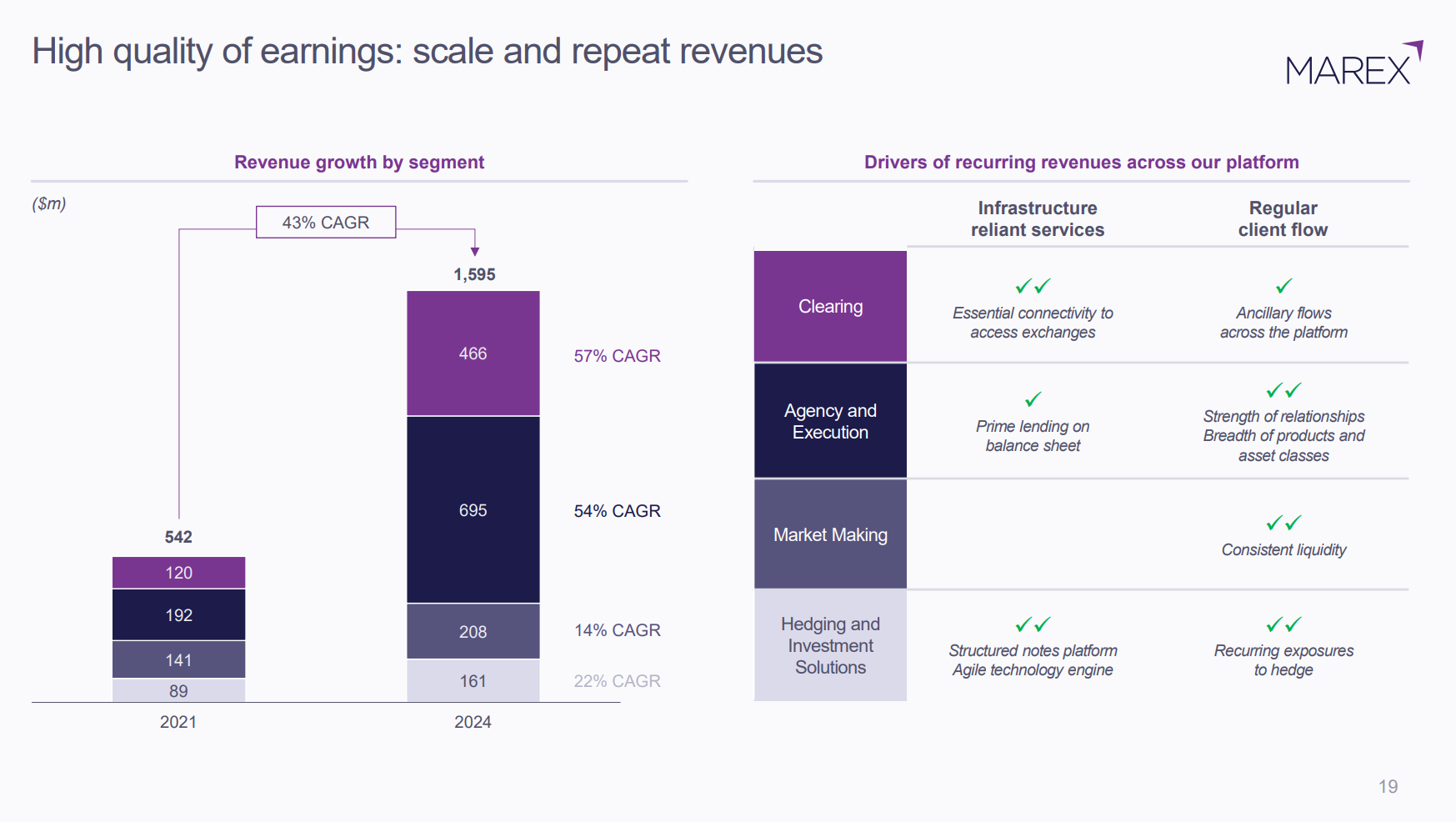

Relatively sticky and recurring services:

Actors within the financial system will always need Marex’s services, whether that’s clearing, execution, market making, or hedging. They provide clearing to a lot of commodities transactions, which I think is a really elegant business to be in - commodity producers and consumers alike all need to hedge their exposure against price fluctuations, which naturally occur every day (and every week, month, and year) in many commodities markets. This means that they have a continual need to hedge, and those trades need clearing, which is where Marex comes in. The best part is, Marex isn’t exposed to commodity price fluctuations themselves, they only help others hedge around those fluctuations, in many different markets around the world.

Execution services (outsourced trading) are also just as necessary and recurring, where Marex will connect client orders (from hedge funds or other large market actors) to pockets of liquidity that they have access to across the globe to complete trades. Similarly, market making will always be necessary, and so will hedging services. Marex provides services that are essentially critical to many different actors who interact within the global financial markets, where they can expect stable, relatively recurring revenue across many different market cycles. Marex takes on low risk for providing any of these services to clients.

Increasing their market share (60% organic growth over time) WHILE making acquisitions and enhancing their own capabilities with those of acquired firms (40% inorganic growth over time). So they’ve got a good organic thing going, and they also know how to do accretive M&A - I personally love to see that.

I still need to do more research on Marex, but from my initial impressions, I think the company could do really well in this market and over time. I really like these sorts of ‘market infrastructure’ businesses (explains my fondness for IBKR as well), because I think they provide essential services that those in the financial ecosystem will always rely on in some way, if not many ways. Both of these companies (IBKR and MRX) generate revenue on a recurring basis whenever people need to trade, hedge, whenever they need liquidity, etc.

People will always need those things, as long as we continue to have a financial system; therefore, I think if you can find a nice company in this space at a decent valuation with a competent management team, you’ve found a nice little compounder with significant long-run tailwinds being, the long term growth of the global financial system. Both IBKR and MRX have diversified revenues across asset classes, across geographies, and they’re well equipped to handle a variety of market cycles. I’m quite pleased to slot MRX in next to IBKR in terms of my little ‘financial infrastructure’ theme. If these companies facilitate access to the market itself, I think the best managed among them can certainly outperform it over time.

Here is a great free writeup on MRX, by Karst Research if you’d like to learn more about the company.

At some point I’d like to own the entire value chain here, from the brokers (IBKR) and clearing houses (MRX), to the exchanges (ICE, - don’t own yet) and everything in between (potentially CBOE, CME, MSCI, and others) - I’m quite bullish on the continued expansion of the global financial system and the dominance of capitalism as a governance system, and all these companies are critical in facilitating that expansion.

I added to my position in VBNK recently (along with a few other positions after a sizeable cash deposit this past week). VBNK is trading very close to tangible book value (over or under TBV by 5 or 10% here) despite the already impressive growth in their newly established US banking arm. To be fair, they did a capital raise not too long ago to support their growing US business, so there’s good enough reason for shares to be depressed, but I still think they’re priced too low. All in, I’m down around 14% on my position today from my cost basis and I plan to continue holding it for a while - I think they could do pretty well into the back half of this year and into next year.

I reduced my position in Kneat (KSI.TO) down to 6%, from ~10%, taking a 5% loss (which is fine really). I think KSI is still attractive long-term, but it’s not cheap today, and after adding Marex I needed to maintain my cash buffer (currently 16.5%).

I also sold my 2% (or thereabouts) position in Gravity Co. (GRVY) for a 5% gain, a game development company with good growth and profitability, but awful capital allocation. They’re trading more or less at net cash because they don’t do anything with their cash, it just piles up on the balance sheet and investors don’t see a nickel - thus their share price has stagnated over the years despite their successful growth. I was interested in GRVY because there’s an activist investor at their parent company, which owns most of their shares; I was hoping that at some point or another, the activist could force the parent to buyout the remainder of GRVY’s shares at a solid premium, capturing a lot of excess value for the parent co. Anyway, I simply lost patience with the stock and decided I could just take the cash or allocate to better opportunities.

The Welfare portfolio continues to outperform the SPY YTD and on a rolling 1-year basis: 6.18% YTD outperformance and 42% rolling 1-year outperformance. I’m up 0.4% over the past week, and down 2.2% over the past month. Not bad! I’ll certainly take the YTD outperformance, even if it’s not by too too much. I’m hoping that my relative outperformance will grow during the rest of the year, helped by a recovery in VBNK shares and continued strength in the other names I own - we’ll see.

Basket performance:

The first baskets I’d like to include in these weekly releases are the Serial Acquirers Basket and the Welfare Diversified Financial Services basket - both newly created. I don’t own any of the serial acquirers yet, though I have been interested in them as an equity class for quite some time.

Welfare Software Serial Acquirers Index (ticker is WSERIAL - follow this index on GoThematic.com once I figure out how to publish it)

Constellation Software (CSU.TO)

Topicus (TOI.V)

Roper Technologies (ROP)

PTC, Inc. (PTC)

Sygnity (SGN)

equal weight, rebalanced quarterly

Wow! I am quite impressed, honestly! That’s some incredibly impressive YTD outperformance from these software acquirers. I was honestly holding off on buying most of them because the valuations aren’t generally cheap per se (though I did flip some CSU shares for 10% earlier this year, randomly), but I guess I was wrong that they might decline in a volatile environment, given their high FCF multiples.

Weekly and monthly performance is 5.11% and 4.88%, respectively. Hell a lot better than my week, I’ll say, haha.

Welfare Diversified Financial Services Index (ticker is WDFINS on Thematic)

Interactive Brokers (IBKR)

VersaBank (VBNK)

International General Insurance (IGIC)

Marex Group (MRX)

Unfortunately Marex isn’t available on Thematic (yet), but for next week’s edition I’ll find a different index creator or go with manual calculations and charts. The below chart does not include Marex, though shares have been surging recently, up 31% YTD, 13% on the week, and 23% over the past month

equal weight, rebalanced quarterly

These are the companies I do own: IBKR, IGIC, and VBNK up until now, and MRX starting this past Friday. You can find great, and free writeups here for VBNK and IGIC from Cluseau Investments. I have a really detailed writeup on IBKR as well, also free to read. These three I’ve owned up until this week, so the relative YTD underperformance for the basket is unsurprising (my other bets like GRND have been carrying me YTD) - though, I think much of the decline is due to weakness in IBKR shares lately, and both VBNK and IBKR shares through the year so far. IGIC has held up really well compared to both of these two. Though if Marex could be included in this chart, I’m sure the returns would be much better, even if I only added it to my portfolio very recently.

Weekly and monthly performance is 5.07% and -0.82%, respectively.

For the coming editions of Welfare Weekly, I’ll begin including relevant news from the week, as well as trade ideas, musings, and financial history tidbits that I find interesting if there isn’t any news to cover. I’ll be adding securities and refining the baskets I cover over time as well - see you all next week!